AE2S Nexus has published the 2019 version of its annual Utility Rate Survey, and the booklets are being distributed to all participants. We would like to thank the 326 participants this year. AE2S Nexus received responses from 132 systems serving populations 5,000 and greater, 151 systems serving populations less than 5,000, and 43 regional rural systems. Survey data was solicited from utilities in Colorado, Iowa, Minnesota, Montana, Nebraska, North Dakota, South Dakota, Utah, Wisconsin, and Wyoming.

Two survey reports have been prepared: one for systems serving 5,000 people or more, including systems in the Minneapolis/St. Paul metro area; and a second survey for systems that serve fewer than 5,000 people, as well as Regional Rural Water Systems. In appreciation for volunteering to provide survey information, each participant receives a hard copy of the complete report.

Reported 2019 Rate Increases

Of the survey respondents serving greater than 5,000 people, 33 are among those in the Minneapolis/St. Paul metro area that receive wastewater services from the Metropolitan Council – Environmental Services. Results from the metro area respondents indicate that 76 percent of the responding systems implemented an increase to water rates in 2019. For the same group, 85 percent of wastewater systems and 84 percent of stormwater systems increased rates in 2019.

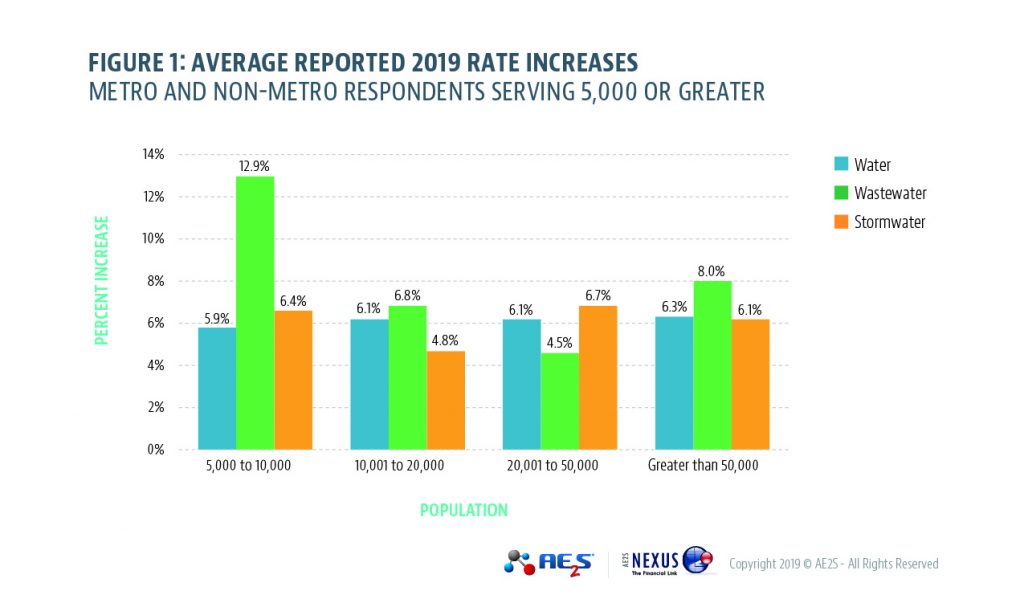

Among the 99 respondents from the non-metro systems serving populations greater than 5,000 people, 55 percent reported water rate increases in 2019, while 53 percent of wastewater systems and 37 percent of stormwater systems increased rates. The average percent increase for each utility by population is shown in Figure 1 for metro and non-metro systems serving 5,000 or more people.

Overall in 2019, the average increases for water, wastewater, and stormwater for systems serving 5,000 people or more were 6.1 percent, 8.1 percent, and 6.1 percent, respectively. For comparison, the average rate increases in 2018 for systems of this size were 5.6 percent for water, 7.2 percent for wastewater, and 16.0 percent for stormwater.

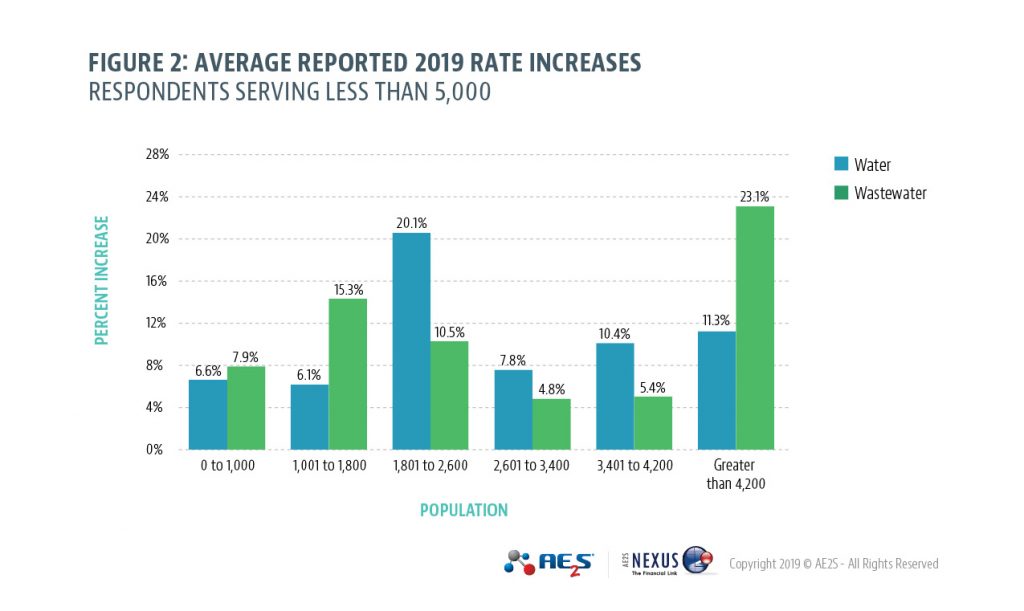

For systems serving fewer than 5,000 people, 32 percent of respondents reported an increase to water rates, 27 percent increased wastewater rates, and only 1 of the 23 systems reported implementing a stormwater rate increase in 2019. For the small systems that reported increases in 2019, Figure 2 illustrates the average water and wastewater increases by population. The stormwater rate is not reported due to the relatively small data set. Among the systems serving fewer than 5,000 people, the average reported increases for water and wastewater rates in 2019 are 8.7 percent and 8.5 percent, respectively. This compares to average increases for water and wastewater of 9.2 percent and 9.0 percent in 2018.

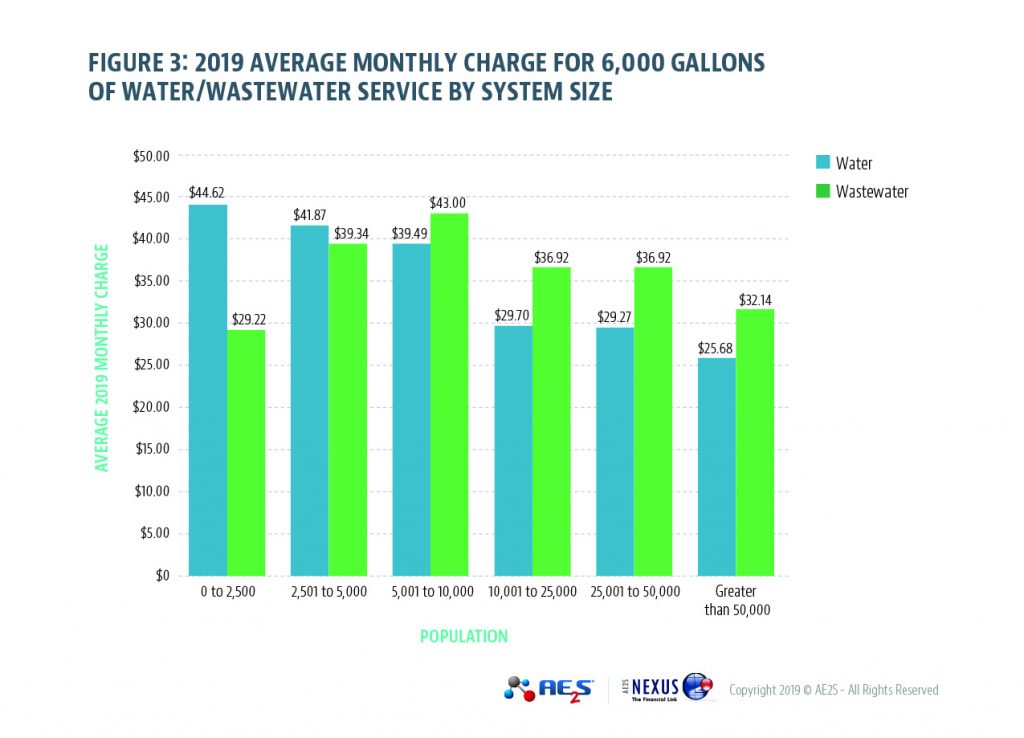

Figure 3 illustrates the 2019 average monthly water and wastewater charges by population grouping for all municipal survey respondents, based on an average monthly use of 6,000 gallons. Of the municipal respondents in 2019, 62 percent also responded in 2018. Overall, the average monthly water and wastewater bill for 6,000 gallons increased by 5.5 percent from 2018, while the median bill for 6,000 gallons increased by 8.3 percent.

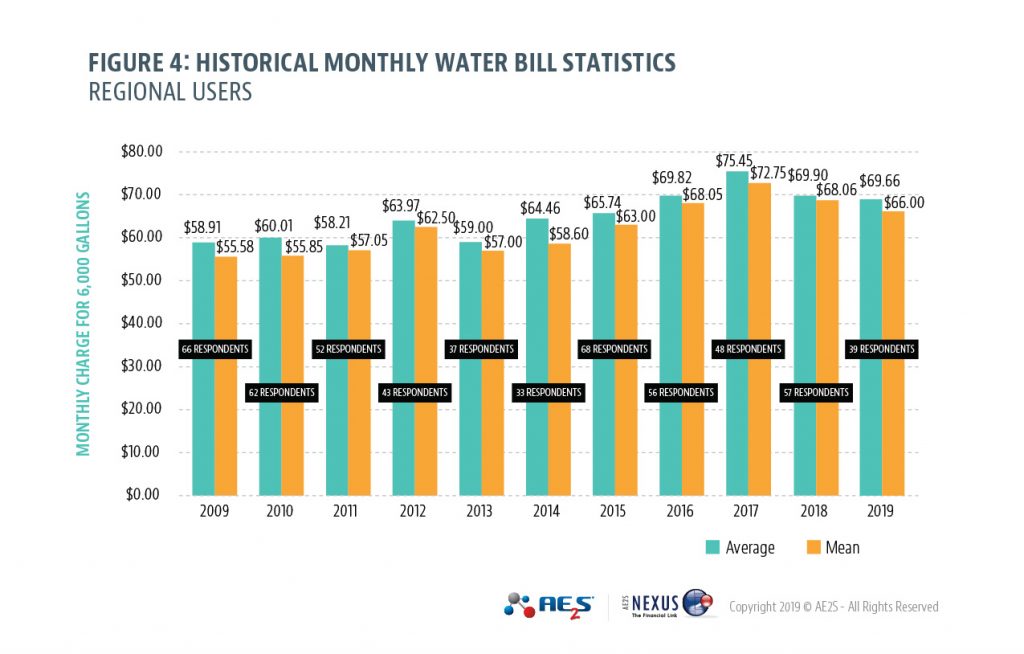

A summary of historical results reported by Regional Rural Water System rate survey participants since 2009 is provided in Figure 4, which shows the average median reported charges for 6,000 gallons of water per month for each year. The number of respondents to the survey each year is also indicated.

Conclusion

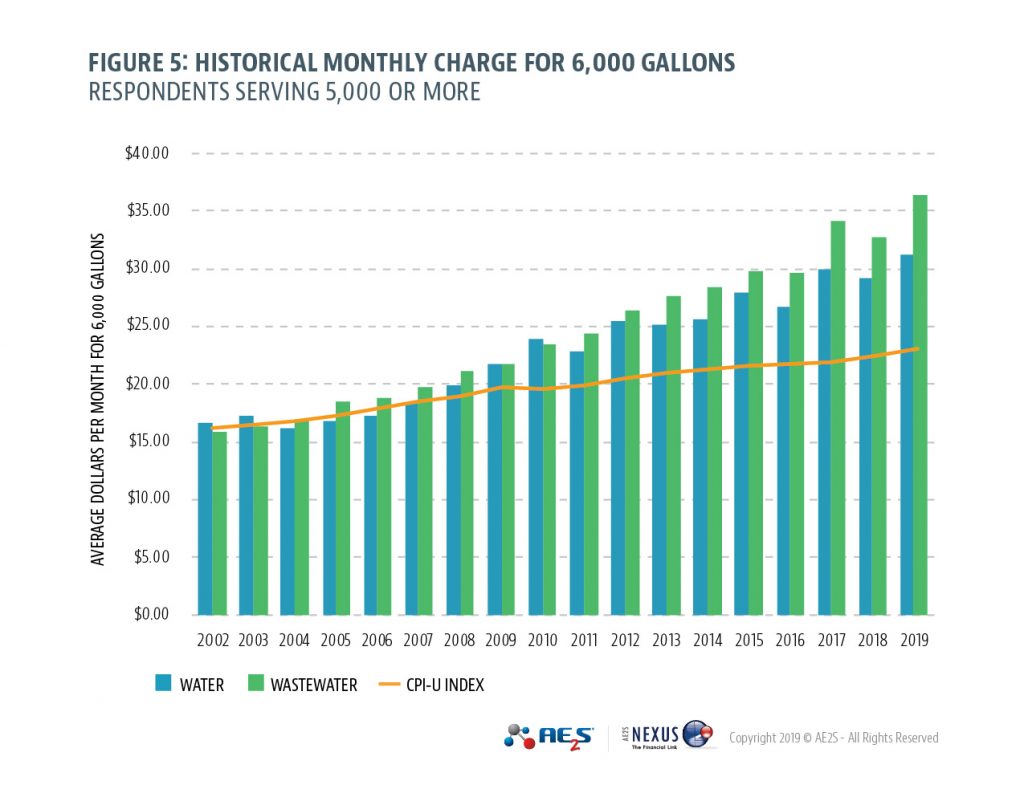

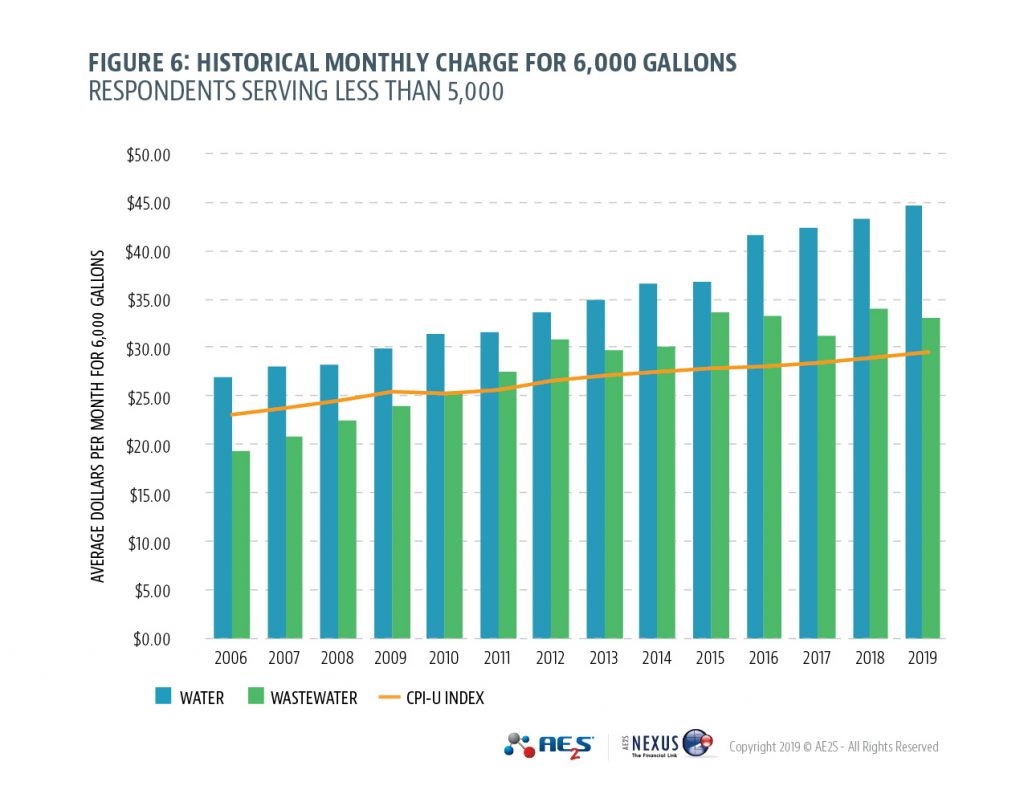

From a historical perspective, the average water and wastewater charge for 6,000 gallons in our region from 2002 to 2019 has climbed at a rate that is considerably higher than inflation, based on the Consumer Price Index for All Urban Consumers (CPI-U). Figure 5 illustrates the change in average charges for 6,000 gallons of water and wastewater service since 2002 for systems serving greater than 5,000 people (including the Minneapolis/St. Paul metro area). Figure 6 indicates similar information for systems serving less than 5,000 people since 2006. The results illustrate the challenge that utility managers and policy makers continue to experience in meeting financial demands for system improvements and operations, while striving to minimize user charge increases.