Utility managers and decision makers know that saving for the future is important. The question is not whether to do it, but to what level. What is the magic number? In the absence of a crystal ball, we are left to estimate future capital investment needs based on a series of assumptions. This becomes a guide for capital reserve planning, which should be considered in the budgeting and rate-setting processes.

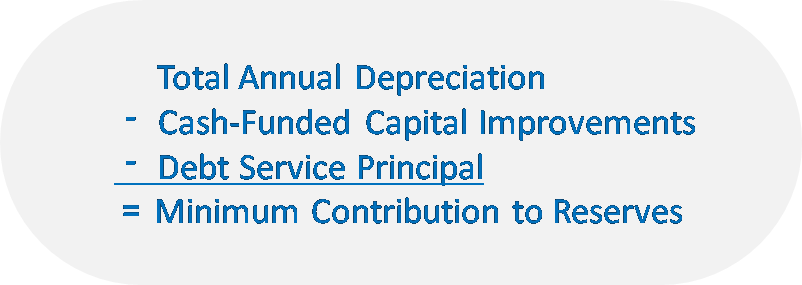

If we back up a bit further, systems sometime fail to initiate reserve planning for lack of understanding where to start. Figure 1 illustrates an entry-level approach to capital reserve planning.

As shown in Figure 1, a system can simply compare the sum of what is being spent annually on in the Capital Improvement Plan (using cash or rate revenue) and on debt service principal payments to annual depreciation reported in the financial statement. If the depreciation value is higher than the sum of the other two values, then a contribution to reserves should be made. If investment in capital improvements and/or debt principal payments are in excess of depreciation, then the system is said to be “funding depreciation” and is meeting at least the minimum level of system investment required.

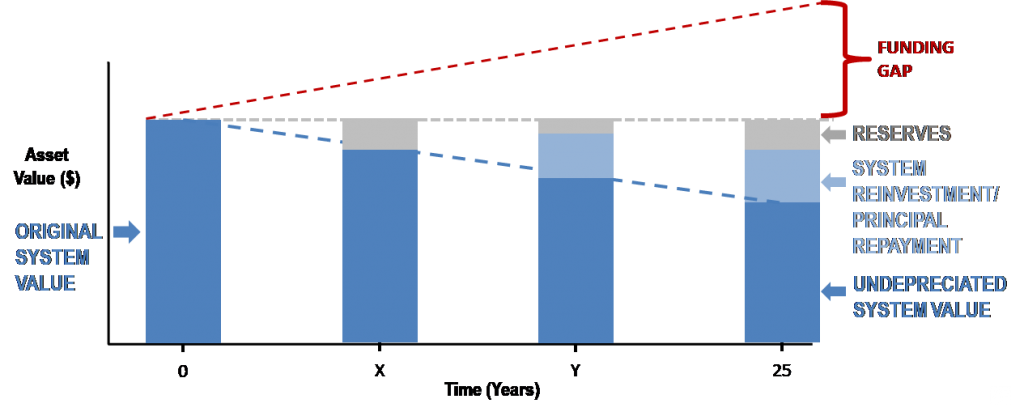

Depreciation is essentially the amortization of the original value of an asset over its intended useful life; however, inflationary impacts are not taken into account. Figure 2 illustrates how even when reinvesting in the system at the level of depreciation, future replacement costs are likely to exceed potential reserve savings due to inflation, even when reserve funds are generating interest. As a result, systems should strive to set reserve funding goals that are based on future replacement costs instead of inflation.

Regardless of the ability for a system to successfully implement replacement-based capital reserve funding goals, understanding the magnitude of future replacement needs is very valuable. Educating policy makers on future financial needs of the system can open the door to implementing rates that provide funds for future capital. Identifying reserve fund targets based on projected needs will help protect those capital reserves from diversion for other uses. It’s a process that often needs gradual implementation, starting with making sure the utility revenues are adequate to “fund deprecation” annually, and working from there.

AE2S Nexus will be speaking about this topic at upcoming conferences listed in the region:

- South Dakota Rural Water’s Annual Technical Conference: January 14-16, 2020 at the Ramkota in Pierre, South Dakota. Kevin Smith will be giving a presentation titled “Water System Depreciation & Responsible Rate Setting” at 10:00 am on Wednesday, January 15 in Amphitheater II.

- North Dakota Rural Water Systems Association 2020 Water System Expo: February 11-13 at the Delta by Marriott in Fargo, North Dakota. Miranda Kleven will be presenting “Water System Depreciation: A Capital Planning Tool for the Well-Managed Utility”. The schedule has not yet been released for this event.

We hope to see you at these or other conferences in 2020 and welcome your questions and discussion on this topic.