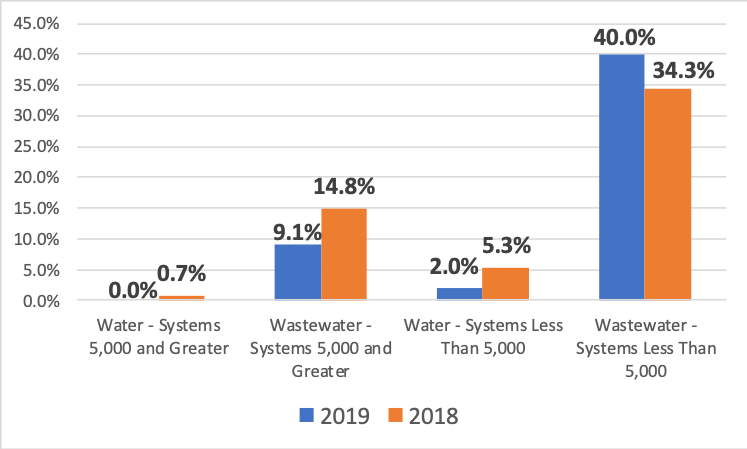

According to the results of the 2019 AE2S Utility Rate Survey, it is most common for systems to utilize a combination of fixed and variable charges in its utility rate structures – particularly for drinking water rates. Just 1.1% of municipal survey respondents of all sizes are using a fixed charge (with no volumetric charge) within the water rate structure, while 25.3% of wastewater respondents reported a fixed charge-only approach.

Figure 1 illustrates the reported 2018 and 2019 statistics for systems reporting a fixed charge-only approach to water and wastewater rate setting. The use of a combination of fixed and volumetric charges provides the ability to balance revenue stability and equitability. Use of a combined approach can also assist in addressing affordability concerns.

The December 2018 issue of The Source presented a discussion of fixed rate considerations. One of the key considerations is the portion of rate revenue requirements to be collected through the fixed charge. A system utilizing only a volumetric charge structure will collect zero percent of its revenue through a fixed charge while a system with only a fixed charge will collect 100%.

Results reported for the 2019 AE2S Utility Rate Survey showed that revenue from fixed water and wastewater charges ranged from 1.7% to 95.8% of annual combined water and wastewater operations and management (O&M) and depreciation costs. For 78 utilities that provided adequate data to perform the calculation, the average revenue generated from the fixed water and wastewater charges as a percentage of total water and wastewater O&M plus depreciation was 37.4% and the median was 35.5%. Industry guidelines suggest 30% as a target for fixed revenue generated to address O&M requirements. This reference does not include fixed revenue designated for debt repayment. Since some of the rates reported in the survey likely contain a component for debt repayment, the results showed that 59% of the reported fixed water and wastewater rates generated revenue exceeding 30% of reported water and wastewater O&M and depreciation.

Equitability Considerations

While annual review of rate performance as it relates to adequate revenue generation is a critical part of the budget process, it is also a good idea to periodically assess the equitability of the rate structure and its impact on low volume users, as well as review how other systems in the region are accomplishing their revenue goals.

The objective of achieving and maintaining rate equitability is usually the reason for completing a comprehensive cost of service analysis (COSA), the basis for which is cost causation – those who cause the cost, pay the cost. While the cost of service is not typically evaluated annually, equitability can be considered more broadly in the context of rate setting and developing annual adjustments to the rates.

Consider a utility is undergoing a project to increase its treatment capacity. The project is likely necessary because some customers require an increased share of capacity at certain times of year. As a result, it would not necessarily be fair to charge every customer the same dollar amount. In the interest of fairness, the cost of increased capacity could be charged to customers in a variety of ways:

- Allocated as a fixed charge based on hydraulic capacity of customer meters by size, to allocate the cost on the basis of potential maximum flow;

- Allocated as a component of the volumetric charge to generate revenue in proportion to the amount of water used; or

- A combination of fixed and volumetric charges.

Now consider replacement of a water tower that is a critical component of core system infrastructure. It could be argued that:

- All users benefit equally from this replacement, justifying a fixed charge per utility bill;

- The benefit is equal on a hydraulic capacity basis and can be appropriately charged on such a basis by meter size;

- As a component of the core infrastructure, it is appropriate to charge on a volumetric basis to generate revenue from each customer in proportion to water used; or

- A combination of fixed and volumetric charges.

The answer will be different for each utility based on system operation and rate-setting philosophy. In evaluating how to develop the fixed and volumetric rate components, it is important to consider that fixed charges can place a disproportionate amount of cost on low-volume users, potentially creating both equitability and affordability concerns.

Affordability Considerations

While fixed charge rate structures can enhance revenue stability, affordability is an important consideration. In addition to potential disproportionate revenue generation, higher fixed charges coupled with lower volumetric charges limit the ability of customers to control their costs through water use.

Earlier this year, new affordability guidelines developed by the American Water Works Association, National Association of Clean Water Agencies, and the Water Environment Federation on behalf of the U.S. Environmental Protection Agency (USEPA) were released.

Though not discussed herein in detail, the guidelines address two metrics as measurement of affordability:

1. Household Burden Indicator – the combined cost of water, wastewater, and stormwater as a percent of the 20th percentile of community household income; and

2. Poverty Prevalence Indicator – the percentage of households at or below 200% of the federal poverty level.

Prior to the new guidelines, affordability was commonly evaluated as a percentage of median household income – a method that the USEPA and industry leaders alike recognized as inadequate. As such, the new guidelines represent important changes that will help systems better assess affordability on a location-specific basis.

Revenue Stability

While fixed charges result in a highly stable revenue stream, a structure with a high reliance on fixed rates is less effective at sending a strong price signal to incent water conservation than a properly structured volumetric rate configuration. While a rate strategy that is heavily dependent on fixed charges may do a good job of meeting near-term revenue requirements, the absence of an incentive to adopt efficient water use practices can drive higher costs in the long-term.

One way to increase fixed revenue without overburdening the fixed charge is to size the first inclining block volumetric tier of water use properly. In many cases, this means capturing all indoor water use in the first tier. Indoor water use does not vary much throughout the year and therefore the first tier of water use will essentially represent fixed revenue.

2019 Benchmarking Data

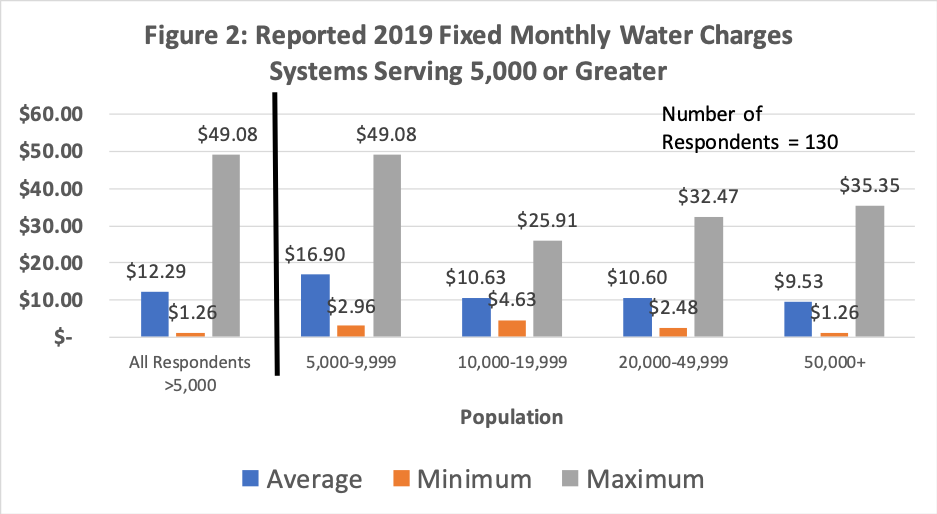

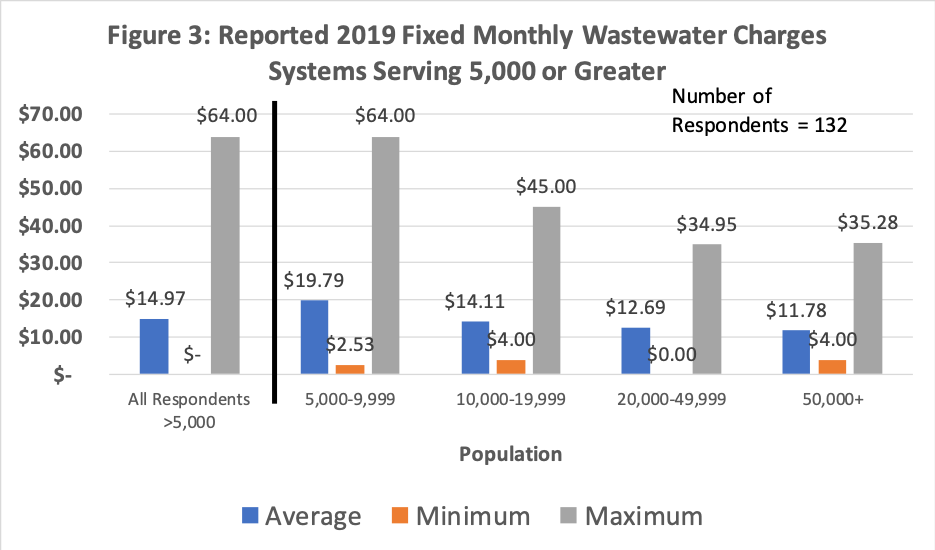

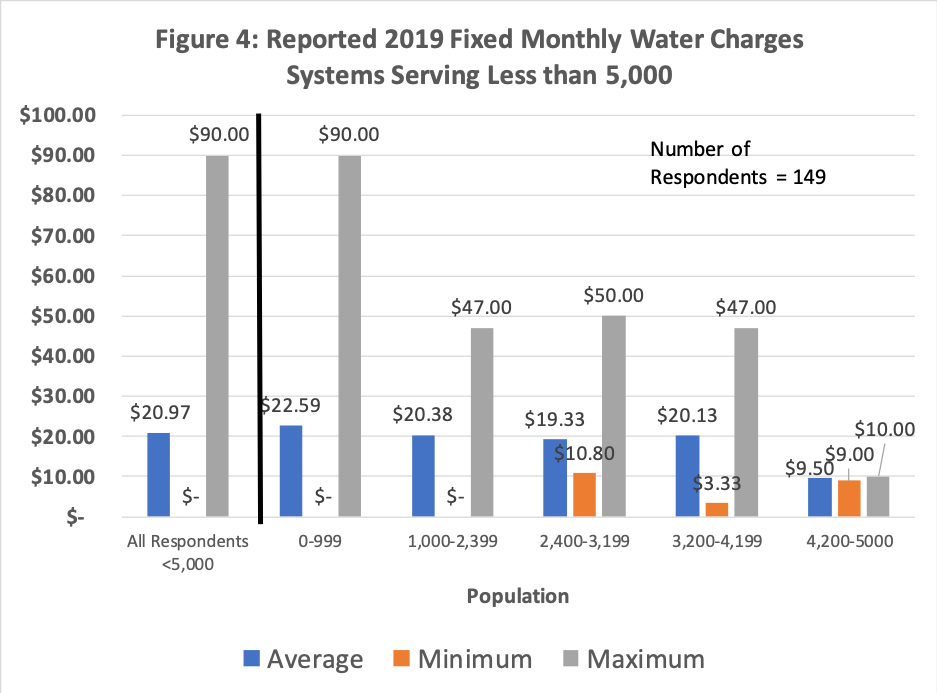

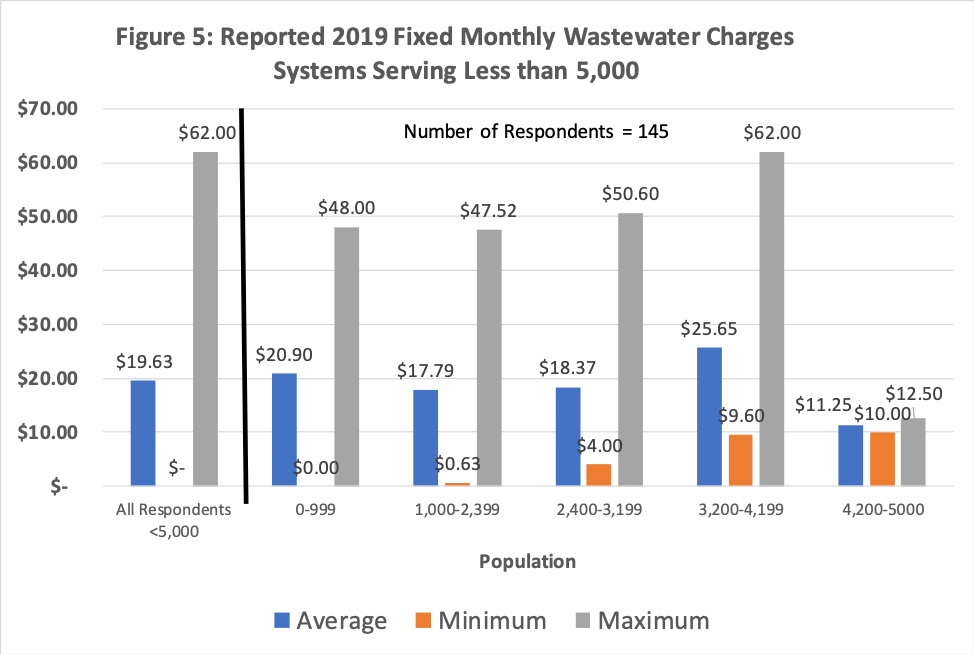

Benchmarking against similar utilities in the region can be useful when considering modifications to your existing rates. Figures 2-5 provide some perspective on fixed charge approaches around the region based on values reported in the 2019 AE2S Utility Rate Survey. Figures 2 and 3 illustrate the average, minimum, and maximum fixed charges reported for water and wastewater systems, respectively, for systems serving 5,000 or more people. Figures 4 and 5 report similar information for systems serving less than 5,000 people.

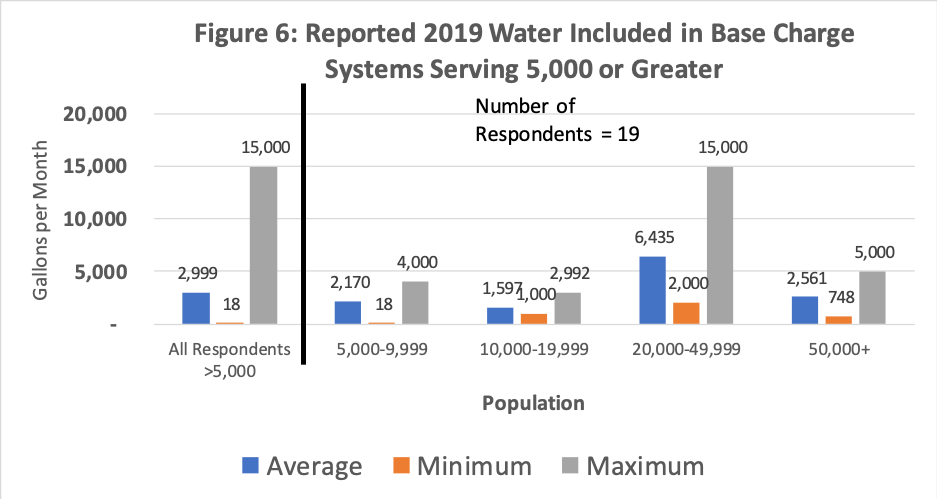

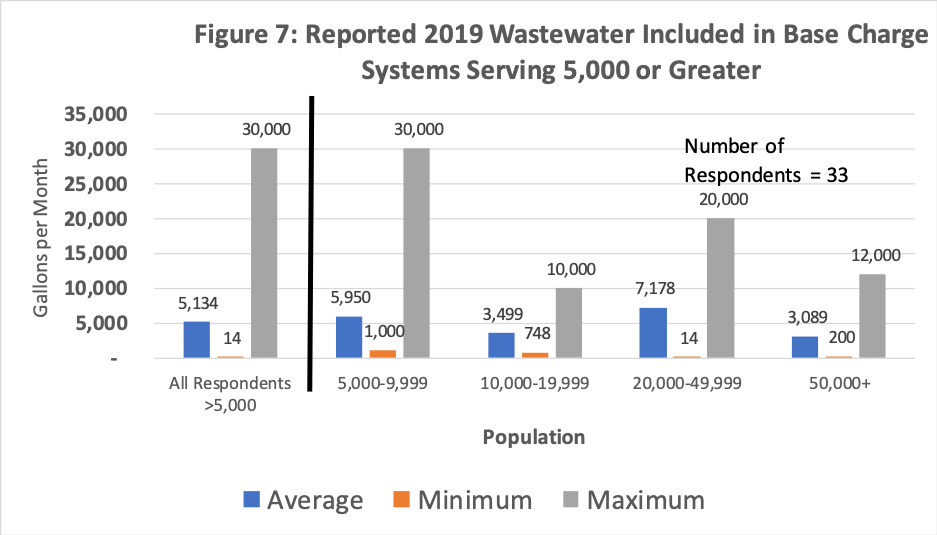

Figures 6 and 7 illustrate the average, minimum, and maximum volumes of water and wastewater, respectively, included with fixed charges as reported by 2019 rate survey respondents serving greater than 5,000 people.

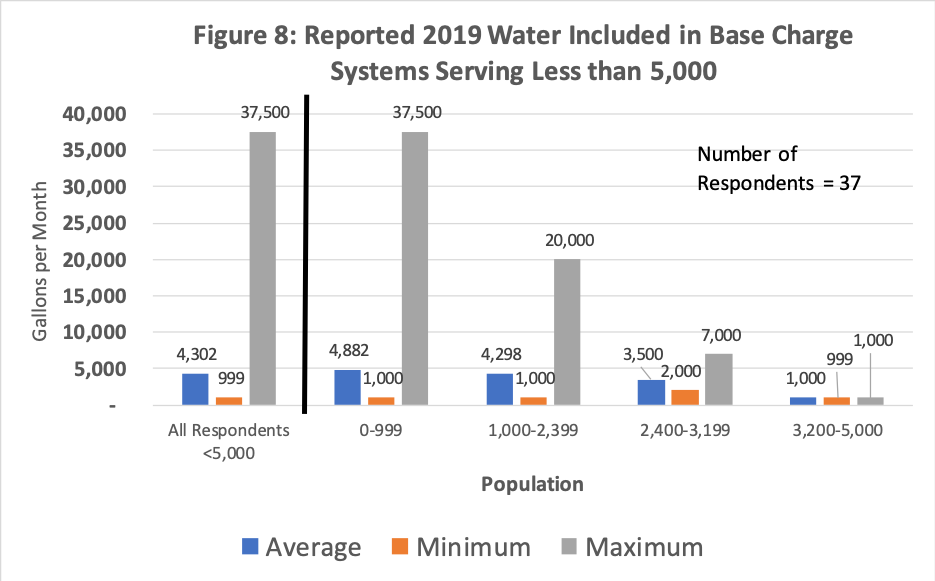

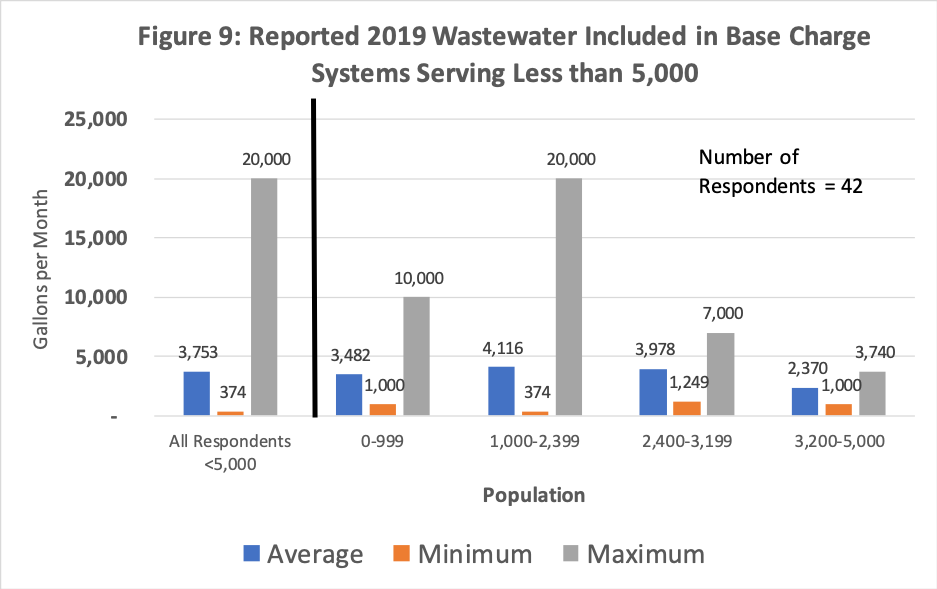

Figures 8 and 9 show similar information for systems serving less than 5,000.

Conclusion

Water and wastewater utilities are challenged to consistently generate revenues adequate to meet revenue requirements, maintain affordable service, and offer service at a rate that is competitive with others in the region. These competing objectives can be difficult to navigate.

Fixed charges provide a steady revenue stream. However, it is important to carefully weigh the impacts of proposed fixed charges in terms of the percentage of total revenue generation, the potential effect on rate equitability, and the impact of fixed charges on low volume users.

When presenting rate adjustments to decision makers, it can be useful to demonstrate how the new rates and the rate structure itself compares to neighboring communities. There may well be significant differences, but that presents an opportunity to further communicate why rates do or do not compare.

Lastly, remember that although near-term revenue requirements are largely fixed and do not vary significantly based on water use, the long-term revenue requirements are driven by customer water use patterns. Failing to signal the cost of treatment and delivery or collection by utilizing some form of volumetric rate structure will result in higher long-term cost for service.

If you have questions about setting utility rates, feel free to contact me at Miranda.Kleven@ae2s.com.